Negative interest rates — logically absurd or mathematically genius?

All financial institutions such as banks, insurance companies, pension funds were all invented and structured on one assumption — positive interest rates.

Credit is built on the basic premise of time differential. It enables you to receive something of value immediately, for which you can pay on a future date. But borrowed money comes at a cost — which is nothing but the interest rate. And this interest rate serves as income for lenders that keeps them going.

Take banks, for instance;

Bank profit = Income earned on interest of loans - Interest paid to depositors.

And this difference forms the pillars of the global banking edifice.

Profit, or no profit, economists weren’t willing to stop at zero. And who can stop economists from coming up with nutty ideas, hence was born the negative interest rate.

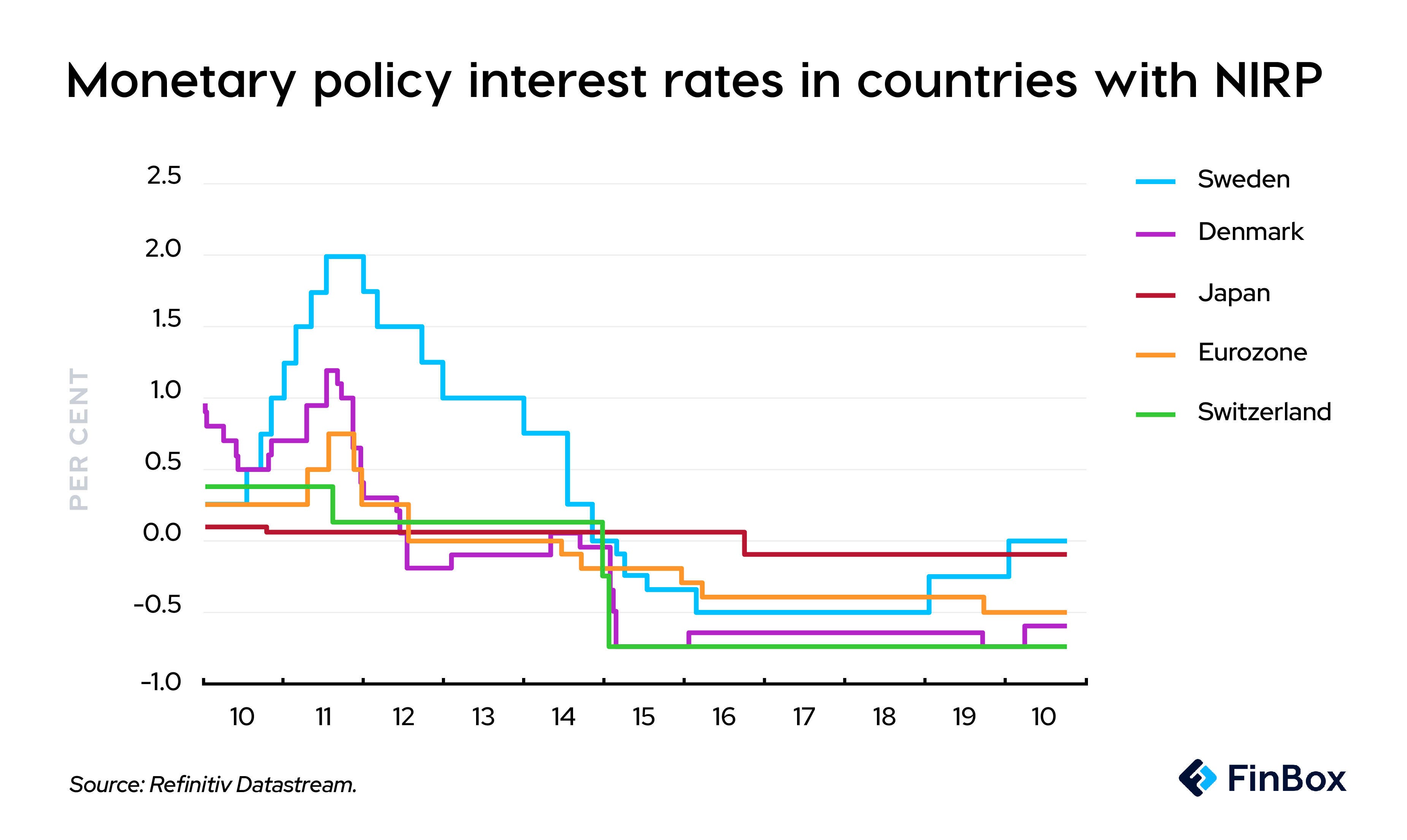

This essentially means that banks will now pay borrowers to take a loan and charge depositors for parking their money with them; it turns conventional wisdom on its head. Such a system, one that rewards borrowers and punishes depositors would have been unimaginable until a decade ago. But today, it is the norm. And currently, 500 million people live in countries with negative interest rates — the eurozone, Switzerland, Denmark, Sweden and Japan.

Surprisingly, savers, including households, did not run to banks to withdraw their cash. There’s no evidence, whatsoever, of cash hoarding in any of these countries. In fact, these countries have had continued decline of cash-use even after implementing sub-zero rates. However, what also needs mention is that a good number of banks in Europe, at least, have refrained from passing on negative rates to retail depositors which they hope will be offset by the reduction in cost of funds.

Why are people willing to pay to hold their money?

Two things come to my mind. One plausible explanation is that the convenience of a cashless society is highly valued by both businesses and households to the extent that it has no bearing on the cost. This offers a ray of hope to banks in India and elsewhere, who are actively investing to deliver a rich digital customer experience, putting short-term profits on the back-burner. Clearly, people are willing to pay for convenience. But how much? That leads us to the next possible reason why cash has still not raised its head.

As I understand it, although the rate cuts have gone below zero, it does not materially affect a saver as much as it does psychologically. For instance, Japan’s rate cut was from a positive 0.05% to a negative 0.10%. Similarly, rate cuts made in other regions as well were both marginal and gradual. Most of us would barely notice an interest-rate reduction of 0.15% on our deposit account, and getting a bank loan for 0.75% less wouldn’t really make many of us rush out to buy new houses. To really boost an economy with an interest rate cut, central banks normally do a lot more.

So, is it possible that rate cuts below 0% could get more drastic? Well, yes they can depending on the goals. Because the very reason why negative rates were introduced in the first place was to spur growth in the backdrop of recession and deflation. If your goal is to get the economy revving, you may have to take the plunge into the negative territory.

Do negative rates make sense?

The answer lies in understanding the difference between nominal and real interest rates. Let’s take the US, for example, whose interest rates are positive but close to zero. In Feb 2022, it recorded an inflation rate of 7.9%. Assuming, you can buy one apple for $1 today i.e 100 apples for $100, and instead of spending you choose to save that $100. A year later, an apple will cost you about $1.08, given the inflation, fetching you only about 92 apples. This means that the real interest rate is -7.9% although the nominal interest rate is close to zero.

On the contrary, let’s take the example of Switzerland who administers a negative interest rate of -0.73% and has had deflation for the longest time. For convenience of calculation, let’s assume the Swiss inflation rate to be -7.9%. Suppose 1 Swiss franc buys you one apple today i.e 100 apples for 100 francs; a year later, 100 francs will fetch you almost 107 apples even after paying a negative interest rate.

The absurdity of negative interest rates makes it hard to wrap your head around the idea. Nevertheless, theoretically, its use as a tool to stimulate the economy to overcome recession/deflation makes sense.

However, when applied to the real world, it spews confusion and is definitely a whole different ball game. Marginal reductions, though below zero, haven't really led countries on the path to recovery. Additionally, supply chain disruptions during the pandemic followed by the Ukraine crisis have shot up prices, with inflation as high as 5.9% in the euro area as of Feb 2022 — a rather precarious situation for monetary authorities.

No real place to make a buck

Until the entry of sub-zero rates, all was going well for banks — except during the Great Depression of 1930, the oil price shock of 1973, Latin American debt crisis of 1970s, the recession of 1980s, Asian financial crisis of 1997, sub-prime crisis of 2008, European sovereign debt crisis that’s been on since 2010, the recent trade wars, the pandemic, and the latest being the Ukraine crisis — just to name a few.

On a serious note, negative interest rates have a profound effect on financial institutions and financial markets, leading to bizarre outcomes. For instance, the interest rate has a direct impact on bond rates. When interest rates are low, bonds that offer fixed yields become attractive. So everybody rallies to buy bonds, driving their prices up and yields down — swinging it far into the negative territory. Yet, the amount of negative-yielding bonds in the global market is $13 trillion, which means people are racing to buy bonds that will pay less than par value on maturity. The logic is if your savings will anyway erode, might as well park it where there’s less erosion.

Basically, no one wants to hold money. Insurance companies would want to pay you back well before you die, pension funds hope you retire early. Turns out banks don’t even want to lend — as the prospect of a risky loan portfolio (due to economic downturn) while margins shrink isn’t the best case scenario.

All said and done, financial institutions have to make money. With negative interest rates barely making a dent on credit offtake, banks have turned to risky assets for making a return. All financial businesses seem to be rushing to the US bond markets to find a positive-yielding bond in hopes of making a buck. Well, negative interest rates have forced players to jettison low- and moderate-risk asset classes, making the whole ecosystem highly risky. It wouldn’t be surprising to see bubbles burst on the secondary market more often.

Technology can lead the way back to lending as a viable business model

Finding low-risk borrowers during an economic slowdown is as tricky as finding a needle in a haystack. For European banks, lending to subprime borrowers during a downturn is literally paying for trouble. Here’s where technology can help.

One, digitisation can drive down operating costs considerably, giving banks a sigh of relief as they face shrinking margins (owing to negative rates on loans and the competitive pressure to maintain positive rates on deposits).

Two, partnerships with fintechs could bake stickiness into financial products that would help cement customer loyalty, creating inelastic demand for products.

Three, new-age underwriting methods that use AI-ML and alternative data will enable lending to even new-to-credit customers at considerably lower risk and significantly lower cost.

Four, opportunities in cash-flow lending and supply-chain lending are plenty. Nearly 80% of eligible assets do not benefit from better working-capital financing, and the remaining one-fifth of assets are often inefficiently financed, according to McKinsey. Here’s a profit pool lying untapped.

Well, the world is talking about shortening the supply chain due to disruptions in long value chains. But that's no easy task. At least a part of the problem can be solved by financial institutions, and in the process they can make gains. How? Extend cash-flow support to businesses facing value-chain disruption through intelligent, targeted financing — enabled by partnerships with fintechs.

In the end, technology can help plug gaps and spur growth through innovation but in a world that’s upside down, there’s a lot more than just negative interest rates lurking on the horizon. How many economists does it take to get the economy revving? Two. One to predict a recession every week and the other to start consuming and hoarding with abandon.

The bottom line

Negative interest rates are theoretically absurd and practically creative! They do pose a rather puzzling set of challenges. Well, every challenge is an opportunity, and whoever said that gave the world a lot more than a cliché.