MSME credit ratings: Dead on arrival?

MSME credit ratings: Dead on arrival?

Not 650, but AAA: Why MSMEs need credit ratings, not scores

Just this week, the Reserve Bank of India’s deputy governor T Rabi Sankar drew the line between fintechs and banks. The former addresses the spatial concerns - such as ease and reach of financial services. Banks plug in the temporal gaps, or the classic case scenario when a borrower’s need for cash does not exactly match a lender’s time of savings. So essentially, banks are the big daddies bringing in the cash when it’s required, and the fintechs just make the whole process easier and digitally savvy.

The equation derails when we bring the micro, small and medium enterprises (MSMEs) in the picture. It’s deplorable that as the fuel for India’s economy - what with MSMEs employing over a hundred million people and contributing upwards of 30% to the GDP - they continue to be the first ones to go under during economic upheavals. Or even during economic stability, they have to continuously stave off working capital crunches and liquidity issues.

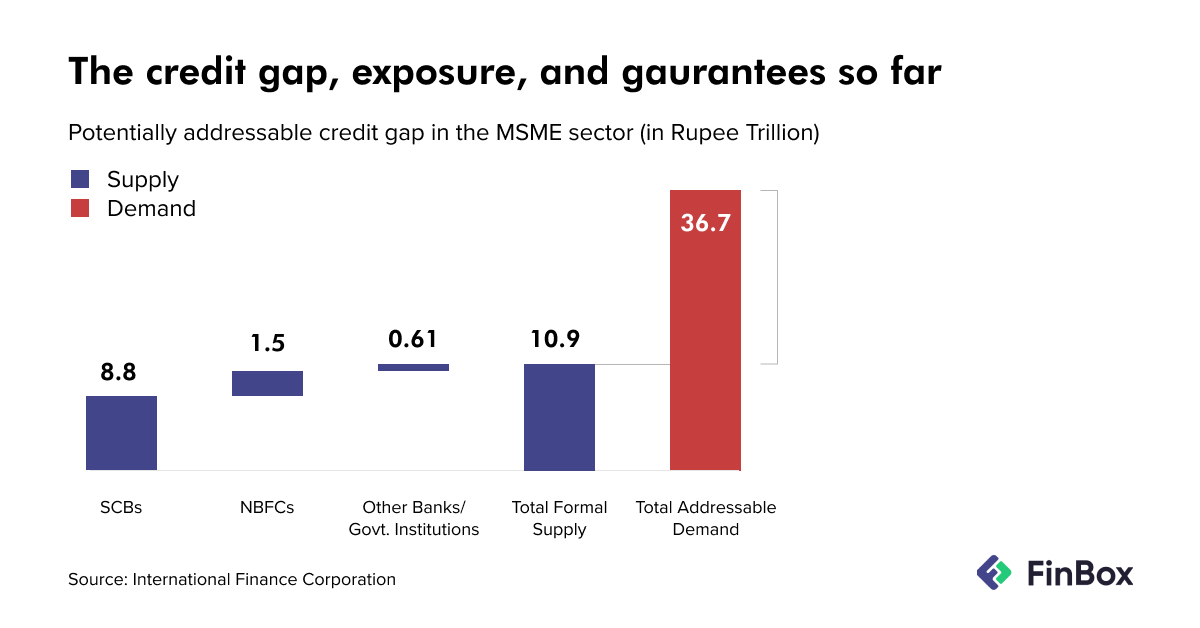

All of which has led to a temporal gap of Rs 25 trillion and banks are not taking the bait. The fintechs, on the other hand, seeing a booming opportunity in the MSME funding space, are trying to bridge the spatial as well as the temporal gaps - by liasoning with non-banking financial institutions and letting technology do it’s thing with alternative data.

These would remain stop-gap measures if banks do not get onboard. They typically shy away from lending to MSMEs for their poor credit scores, because a small kirana shop couldn’t possibly have top-notch accounting records, well-audited financial statements or a stellar business plan. And if they do get lent to, they pay higher interest rates to factor in the risk and sometimes, even the bias.

The real issue here? The models that banks deploy to assess a small business - if they even get that far, given the opportunity cost of not lending remains laughably low. These models or algorithms are designed for the big corporations, with swathes of neatly done data sheets and impeccable records stored in software sourced from the likes of Oracle or SAP. This level of standardized assessment just makes life easier for banks.

For MSMEs, however, this model is unfavourably biased.

The fix? Not credit scores, but credit ratings. Something like what a S&P Global or Moody’s does for the big guns. But using their models to assess MSMEs will be the old wine in a new bottle. The credit rating for MSMEs needs to be custom-built, holistic, granular and even would involve physical visits and audits. An agency that takes up the task would need to source point data - something that continues to plague India’s digitally-nascent economy - and turn it around into a rating that banks can work with. The model here should factor in the unique business, financial, operational and management risks - embedded in context and built for purpose.

If such a credit rating system props up in India, it would help MSMEs secure loans at interest rates commensurate with their business, and would help banks capitalize on a new customer base, without incurring exceptionally high transaction costs. Needless to say, the non-performing loans that MSMEs have been notoriously associated with, will reduce because decisions are now made on data and not under government duress. A credit rating system will also help bring some of the operational sanity to small businesses, pushing them to clean up and maintain records, be compliant for audit trails and pivot to a digitized mode of storing data that will open so many avenues.

Something like this was in the offing in December 2019, when the then MSME minister Nitin Gadkari hinted at a credit rating agency for MSMEs. That seems to have been put on a back burner, despite doubling of the MSME loan accounts restructured under the COVID resolution schemes. We don’t know why.

We only know it makes sense to do it, and fintechs - with their spatial role - can help gather the data and even crunch it - should an agency like that see the light of the day. And it should bring a sector - that employs a hundred million people and contributes to 30% of the economy - out of the shadows of shadow lending. The question is, who will finally bell this cat?