LIC: The rare blue diamond?

The mother of all listings — the LIC IPO — is just around the corner. Last week, LIC filed Draft Red Herring Prospectus with SEBI, seeking approval for its IPO. The embedded value of this 65-year old legacy institution soared more than five times in six months, creating a stir that’s typical of a technology startup that joined the unicorn club. If it hits the numbers, then it would surpass the biggest Indian IPO to date — Paytm's $2.5 billion listing.

Sheer back-of-the-envelope calculations would suffice to know that LIC against other Indian insurers is akin to Gulliver in Lilliput. Delve deeper, and you know that Gulliver is not all that big as it first appears.

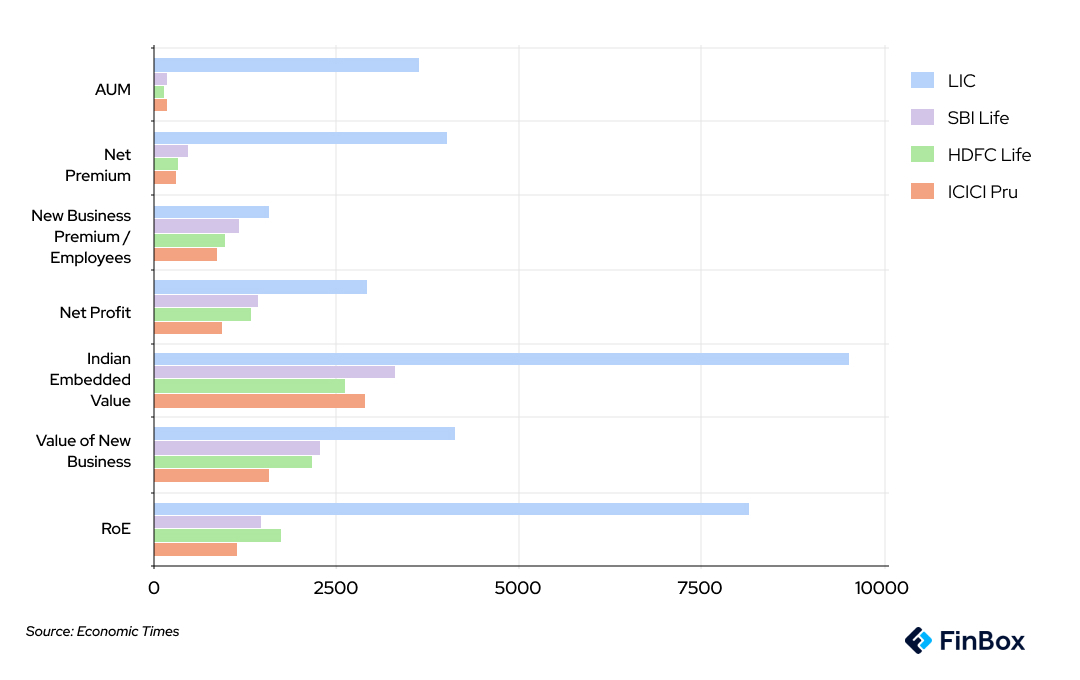

Let’s first look at the giant that LIC is and see how it fares against other players in the Indian insurance market.

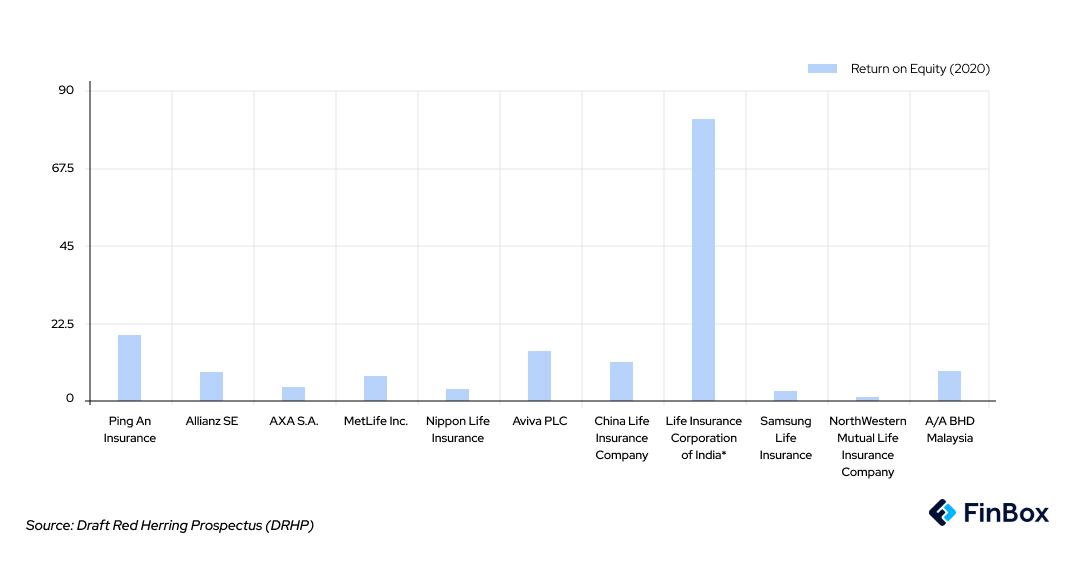

The above chart clearly indicates how LIC towers over other domestic insurers on several parameters. However, one metric that truly matters to investors is Return on Equity (RoE) — a measure of the company’s profitability. The above chart shows how LIC’s RoE of 81.7% makes other domestic players’ look so small in terms of ability to produce a return on investment (SBI Life: 15.2%, HDFC Life: 17.6%, ICICI Prudential: 11.7%). That’s not all, it had the highest RoE among global peers as well in fiscal 2021 (see the chart below).

LIC’s RoE stands tall at 82% followed by Ping An Insurance (19.5%), Aviva PLC (14.8%) and China Life Insurance (11.9%); four times its nearest competitor.

What explains such an unmatched, unrivaled RoE?

It could be one of two reasons; either LIC is a model for the world on how to use investments with utmost efficiency, or the metric hides more than it reveals. The former is unlikely, for the world would have swooned over this profit-minting business model by now.

So, let’s look at how RoE is arrived at.

Simply put, RoE is net profit divided by net worth (assets minus liabilities). In this case, it has been calculated by dividing ‘profit after tax’ with ‘average equity of fiscal years 2021 and 2020’.

Either of two factors can drive the final RoE value; a high-value numerator or a low-value denominator. In fact, LIC has a reported net profit (numerator) of only ₹29 bn in FY21 despite a very large AUM (Assets under management) of ₹39.55 tn as of March 2021. This reported net profit is seemingly highly understated and does not capture the true earning potential of LIC. However, what's clear is that this inflated RoE is the influence of the denominator.

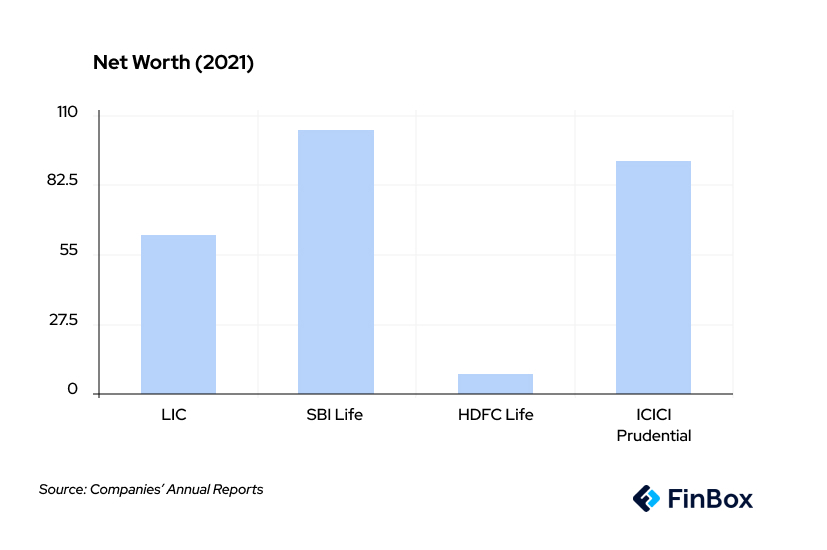

LIC’s reported net worth stood at ₹63.6 bn and ₹7.4 bn in FY 21 FY 20 respectively. The average net worth of the two fiscals amounts to ₹35.5 bn which is extremely low in comparison to its peers (see the chart below).

To put this into perspective, LIC’s AUM was more than 3.3 times the total AUM of all domestic private life insurers put together and more than 1.1 times the entire Indian mutual fund industry’s AUM (Source: Livemint). Hence, given the size of the enterprise, this reported net worth is rather minuscule.

The reason for such low levels of reported net worth can be attributed to some unique aspects that set it apart from other players in the market.

LIC — the rare polka-dotted zebra

First of all, LIC cannot be compared to other players on an equal footing owing to its unique governance structure. It is additionally governed by the LIC Act 1956 and LIC Regulations 1959 on top of the Insurance Act 1938 and Insurance Regulatory and Development Authority Act 1999. This resulted in a bit of a hotchpotch, curtailing its operational flexibility. The Finance Bill 2021 passed 27 amendments to align it closer to the way private players operate.

LIC’s reported net worth is a highly diminished value, unlike other private players. This is because its surplus policy required it to distribute 95% of its surplus to policyholders and 100% of its net profit as dividends to shareholders (in this case, the government).

Recently this policy was modified and its share capital was increased, which explains the jump in reported net worth from ₹7.4 bn in 2020 to ₹63.6 bn in 2021.

As per the earlier policy, 95% of the surplus had to be shared with participating policyholders and only 5% with shareholders. In addition, LIC used to operate a single control fund, unlike private players which meant that any surplus that was created in non-par business (largely annuity and group business) was parked back in the single fund which was available for surplus distribution to the par policyholders. This would make any investor wary. However, the government is trying to bring parity.

Another reason why the net worth of LIC is currently low is because of its narrow capital base of just ₹100 crores. A decade ago, it was just ₹5 crore. It is clearly undercapitalized — typical of government institutions. And IRDAI has not forced it to increase the base because of the LIC Act and the sovereign guarantee (there is no solvency risk) (Source: Business Today). Well, all this has clearly influenced the RoE ratio’s denominator culminating in a classic case of ratio bias. There's safety in numbers, but, evidently, only up to a certain extent.

Summing-up

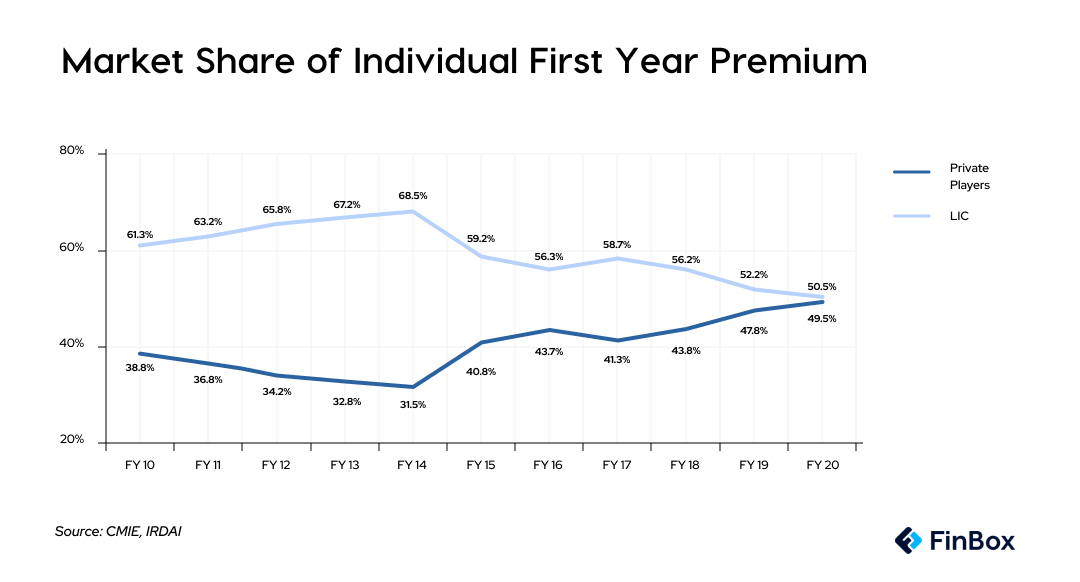

LIC continues to be a market leader in traditional segments but has not gained market share in newer segments like Unit-linked Insurance Plans (ULIPs). While it enjoys benefits of size, a network of agents, and historic branding, in matters of digitisation of its business, it ranks lower than private players. This is evident from the market share erosion it has been experiencing, especially during the pandemic.

While the IPO’s fate is yet to be revealed, LIC is bound to face intense competition as its peers digitize and drive their profitability upwards (see the chart above). Being agency- and channel-driven, LIC lost considerable market share during the pandemic. To learn how digitization is changing the inclusion paradigm, read our blog.

By mandating segregation of investment portfolios between par and non-par businesses and increasing the share of surpluses in investment returns to shareholders, LIC’s books are only now starting to become comparable with that of the other players. Once it finally hits the public markets, the rubber will hit the road and we’ll perhaps have a better chance of making sense of and learning from this insurance behemoth.