Can digital credit finally light up this Diwali?

Can digital credit finally light up this Diwali?

This Diwali, Indians will revenge spend. Who’s up for funding it?

India’s festive season, or the run-up to Diwali, is the make-or-break moment. The usually thrifty Indian households let loose their purse strings and tend to splurge on non-discretionary items (often delaying big-ticket purchases such as air conditioners, washing machines or automobiles for Diwali). Giving a boost to the festive frenzy are retailers - both foreign and home-grown, online and offline - doling out competitive deals across categories such as fashion, electronics, household appliances, you name it.

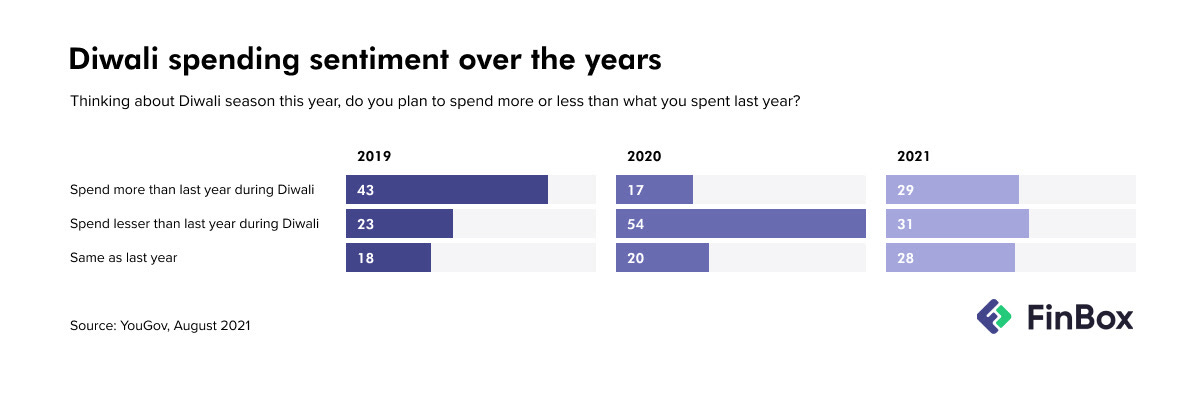

This year, that marks the two-year hiatus to the Diwali fervour, looks extra promising. Retailers anticipate pent-up consumer demand to spur ‘revenge spending’ - or the making up for the lost time under COVID-induced lockdowns and the time that would be lost should a third wave hit. There certainly is a shift in consumer spending, after a debilitating second wave that gripped India in the April-June quarter of this year. Yet, the festive spirit is reviving, though it certainly has not rebounded to pre-COVID levels.

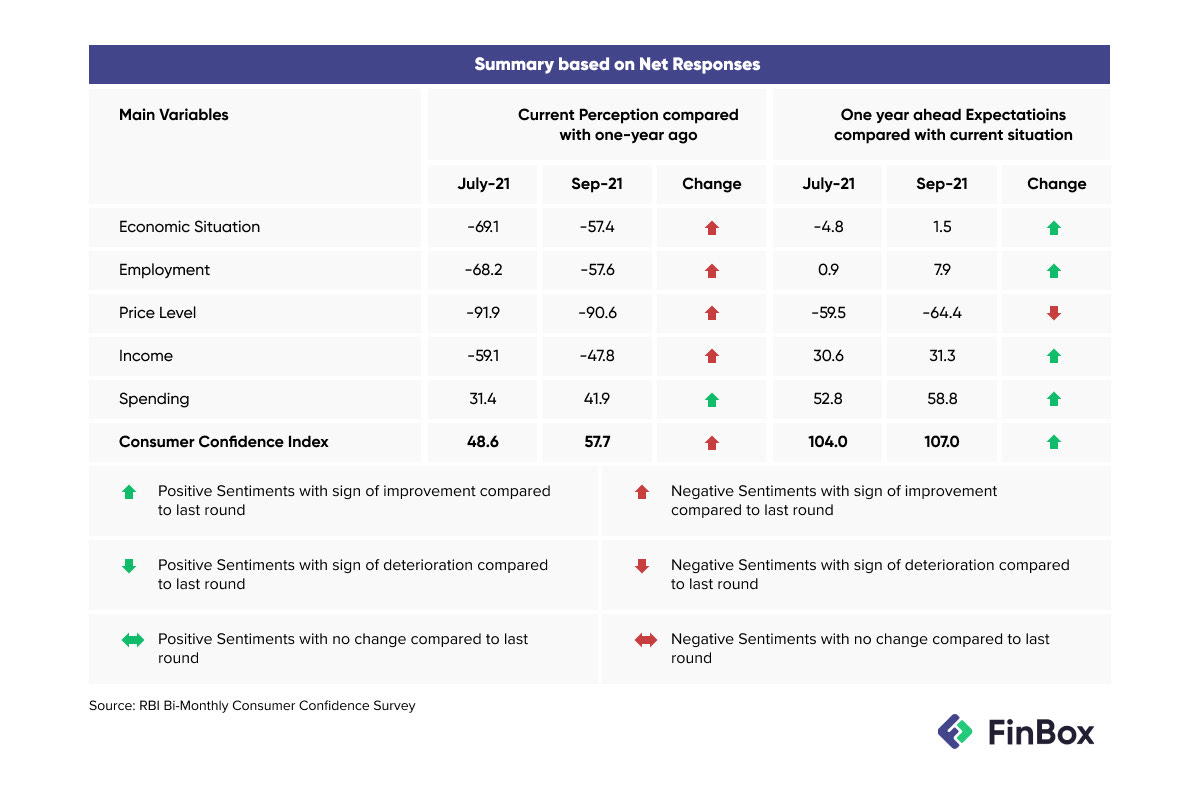

These numbers need to be seen in a broader context, given employment, income and inflation levels are yet to improve (see figure below). Spending is the only indicator to stay robust in an economy which is far from being out of the woods.

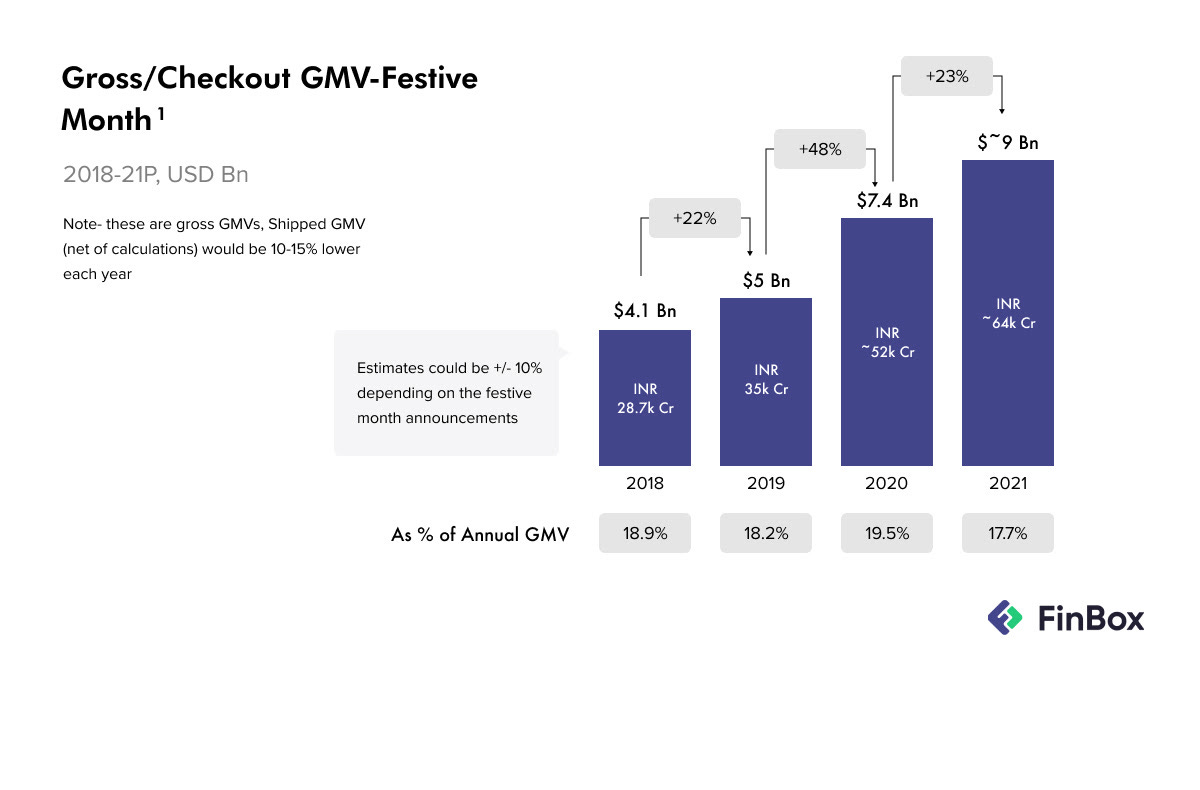

A Forrester study pegs India’s online sales to reach $10 billion this Diwali, a 42% increase from the previous year, with 50 million of the total 75 million online shoppers coming from tier-2 or 3 cities.

With Indians throwing caution to the wind, what's financing the festive frenzy? It’s the strides made in the embedded lending space, specially by online giants Amazon and Flipkart. Point-of-sale credit options such as buy-now-pay-later continue to be on an assured climb, with trends pointing to a 10-fold jump in transactions made through this payment option. Amazon and Flipkart are hoping to cash in on the ubiquity of digital payments and the inroads made so far with easy credit options, clocking $2.7 billion of gross merchandise value in the first four days of the online sale. Nearly half of it came from smartphones.

The FinTech imperative

The credit-frenzy and BNPL popularity hasn't come about as a chance happening but instead is a work of FinTech mindset gaining popularity. Due to the penetration of FinTech experiences such as wallets and UPI, customers have come to expect the same speed and ease of checkout and shopping - whether it is online or offline.

Enter solutions like BNPL, checkout financing, and credit lines which are helping platforms prequalify borrowers, asses risk in a jiffy, and directly offer credit at a cart level. This brings down the drop-off rates down to half, according to internal FinBox data.

At the same time, it also boosts sales numbers for the platforms as the consumer affordability increases as multiple price points come under budget with the option of splitting payments over a period than paying it all at once.

This Diwali, Arzooo, a B2B retail technology startup that has partnered with FinBox for its credit offerings, plans to disburse Rs 300 billion as unsecured credit to small offline consumer durable retailers. This will help offline retailers, especially in tier 2-3 cities, to clock in higher sales and take a pie out of the festive churn. Arzooo is looking at a 22-times jump in sales via its platform - all backed by credit lines it extends to its clients.

If trends hold, this will be the bumper Diwali Indian retailers. For lenders as well, who end up making 12% (ballpark) of each BNPL plan opted for via an aggregator platform, this is a bounty they chanced upon. It’s a Happy Diwali for everyone.

If you are FOMO-ing, it isn’t too late to get on the embedded lending bandwagon. FinBox can get you up and running within a fortnight, just like we helped Arzooo. Our end-to-end embedded finance technology stack abstracts the complexity of assessing borrowers and credit risk, helping you tap into the next billion. Let’s talk!